The Permitting Paradox

Why the Cynics are Misreading the EU’s Raw Materials Statecraft

By Nicholas Vafeas

Published 22 May 2026

At a Glance

The Reality: European mineral security is routinely dismissed by critics as slow, buried in red tape, and structurally outmatched by China's multi-decade head start.

The Complication: The legacy model of relying on passive, open markets is completely broken, leaving Western supply lines vulnerable to deep geopolitical friction, asymmetric foreign mining laws, and hostile regional bottlenecks.

The Strategy: Driven by the Critical Raw Materials Act (CRMA), the EU is successfully transitioning into a sovereign economic actor—systematically building defense shields through industrial waste valorisation, institutional project de-risking, and centralized, pan-European strategic stockpiling.

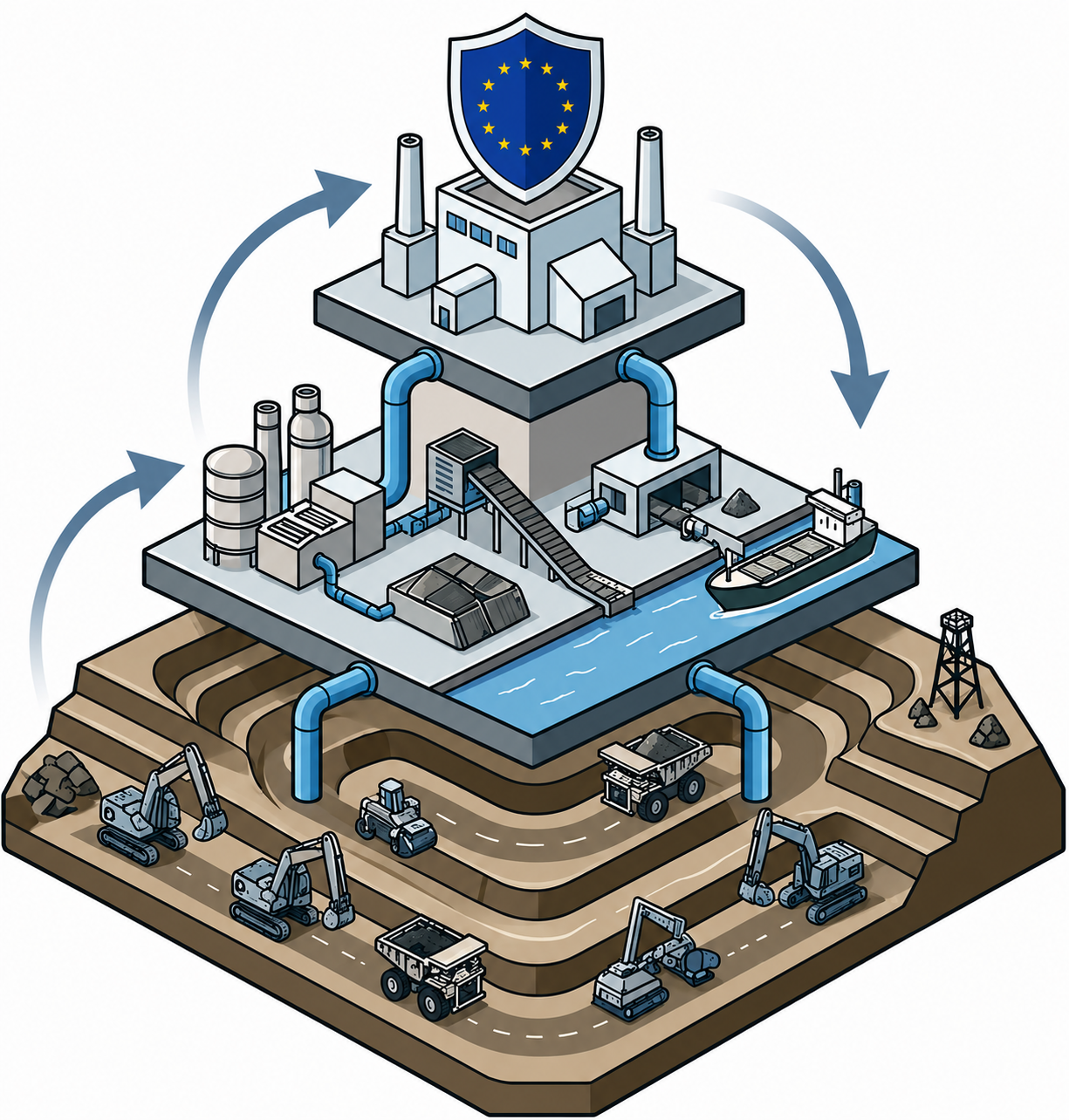

A conceptual systemic architecture of the EU Critical Raw Materials Act (CRMA). The model contrasts traditional open-cast primary extraction layers with an integrated midstream loop featuring industrial waste valorisation, secure maritime logistics, and localized processing infrastructure, all anchored under a unified, defensive pan-European security shield.

We have a bad habit in the West of treating mineral exploration with euphoric hysteria. During a lithium boom, every outcropping pegmatite is suddenly branded a potential payday. And now it seems to be rare earth’s turn. But when the market cools or bureaucracy stalls (and the mining cycle always does), the pendulum swings instantly to cynical despair.

Critics have spent months picking the strategy apart. The narrative is easy to sell, and it sounds reasonable on the surface: “Europe is bogged down by red tape”, “outmatched by China's multi-decade head start”, “structurally incapable of competing in heavy industry”. High-profile commentary often highlights these structural stalls, framing Europe as fundamentally broken for industrial development.

But, (and let me make this absolutely clear) this perspective falls into a dangerous trap, because it mistakes incomplete visibility for structural failure. In the raw materials space, complexity is often just a symptom of looking at individual pieces rather than the entire architecture of the system. Granted, confusing transparency is, in itself, a systematic issue too.

When we put aside our cultural desire to critique, zoom out, and look at the system-level shifts that have occurred since the Critical Raw Materials Act (CRMA) was published, we start to see a different picture. The EU isn’t just writing defensive policy, it is fundamentally changing its approach to resource governance. For the first time (and it did take a long time!), the Bloc is transitioning from a passive, market-driven buyer into an active player executing deliberate economic plays.

The Geopolitical Crucible: Why the System Had to Change

To understand why the EU’s progress matters, we have to look honestly at the realities of global resource competition. The old model (i.e. relying entirely on an open, unhedged market that rewards the absolute lowest cost of extraction) is dead.

Consider the current geopolitical chessboard:

The Central Asian Bottleneck: Roughly 70% of Central Asia’s critical mineral output currently flows directly to China. Western diplomatic efforts to secure alternative supply lines in the region are met with immediate friction, with Russia openly treating the West’s critical mineral push as an aggressive intrusion into its geographical "backyard."

Asymmetric Legal Adjustments: Competitors aren’t operating on static rules. China recently executed quiet, highly strategic revisions to its domestic mining laws, deliberately tightening state control over mineral exploration, production, and technology exports to maintain its dominance.

Alternative Processing Nodes: Regional midstream players are rapidly organizing. Türkiye, for example, is aggressively positioning itself as a geopolitical alternative processing hub, aiming to intercept raw flows from Central Asia before they reach either Eastern or Western megamarkets.

In this environment, predictability is everything. If Europe remained a fragmented group of twenty-seven individual nations trying to outbid each other on the open market, its industrial base would face eventual defeat. The energy transition does not care about your policy ideals, it cares about resilience and secure delivery over decades.

Strength 1: Designing for By-Product Innovation and Waste Valorisation

One of the biggest, yet underappreciated strengths of the EU's raw materials policy framework is its explicitly tailored approach to geology and technical reality.

The market often chases simple, high-grade Greenfield discoveries. But Europe’s primary advantage lies in its massive, highly mature industrial footprint and its ability to target secondary/waste resources. The CRMA formally mandates this by requiring that operators of existing and new extractive waste facilities conduct preliminary economic assessments to recover critical minerals from their waste tailing ponds. And we are seeing this exact system-level design play out on the ground in Finland. Terrafame is currently evaluating the feasibility of extracting scandium directly from the secondary processing streams of its uranium and polymetallic operations.

I’ve mentioned this before, but scandium is a textbook example of a structural bottleneck, highly critical for aerospace alloys and solid oxide fuel cells, but notoriously difficult to find in stand-alone primary deposits. Rather than waiting a decade for an entirely new primary mine to pass environmental permitting, Europe is leveraging its existing infrastructure. If successful, Terrafame will become Europe’s sole domestic supplier of the metal, bypassing traditional exploration lead times.

Strength 2: Financial De-Risking and Bilateral Agreements

Of course, a strategy is only as strong as the capital backing it. Critics tend to argue that European public funding is too fragmented to match the state-backed balance sheets of global rivals. However, this view completely misses the targeted coordination taking place between member-state capital, federal policy, and international asset developers.

Look at the ways in which Germany is securing its midstream supply chain. Germany’s Federal Institute for Geosciences and Natural Resources (BGR) recently completed an extensive technical assessment of NextSource Materials’ Molo graphite mine in Madagascar. This was not a superficial academic review, it was a targeted de-risking exercise linked directly to Germany’s €1 billion Raw Materials Fund (Rohstofffonds).

This represents a highly pragmatic blueprint for external diversification. While some regions experiment with defensive, retroactive trade barriers (such as the volatile tariff environment seen in Brazil's 2024 EV market), Europe is playing a more resilient long-term game. By using institutional technical bodies to validate international projects early, the Bloc is securing the baseline raw material inputs before they are processed into downstream components.

Strength 3: The Blueprint for Collective Security and Stockpiling

The true test of any geopolitical bloc is its willingness to pool sovereignty for defensive resilience. Historically, the EU left mineral stockpiling to the discretion of individual member states, creating enormously visible single-point vulnerabilities. The CRMA structurally corrects this coordination problem by introducing unified monitoring and centralised, defensive buffer frameworks. The Bloc has officially shortlisted highly vulnerable, highly concentrated critical minerals (including tungsten, rare earth permanent magnets, and gallium) for its inaugural coordinated strategic stockpiling mechanism.

This completely rewrites the risk profile for European advanced manufacturing. An export ban that might have crippled an isolated industrial cluster in western Europe can now be absorbed by a coordinated, pan-European strategic buffer.

The Architecture is Solid. Execution is the Only Benchmark.

Overall, the majority of criticism likely stems from impatience, particularly when seeing other external nations rapidly execute policies without delays (and in some cases, without regard for socio-environmental concerns). But the EU’s critical raw materials strategy should not be evaluated on whether it can recreate a state-dictated, closed-loop economic model. It should be judged on how effectively it leverages a democratic, multi-state system to achieve industrial security.

Building a resilient supply chain from scratch is a decades-long task, and bureaucratic delays remain a persistent (and painful) threat. But the underlying policy engine does have teeth. Europe is no longer wandering aimlessly through the global mineral landscape, praying for a lucky discovery. It has recognized its dependence and is systematically creating its own security.